EU approved new sustainability reporting rules

The European Parliament approved final simplified rules for sustainability reporting and due diligence. From now on, only companies with more than 1,000 employees and an annual turnover above 450 million EUR will be subject to reporting obligations. Due diligence must be implemented only by companies with more than 5,000 employees and an annual turnover exceeding 1.5 billion EUR.

Members of the European Parliament approved on Tuesday, 16 December 2025, the final adjustment of the requirements for implementing sustainability principles into the operations of companies operating in EU countries. This step follows the adoption of the Omnibus I package, with which the European Commission launched in February 2025 measures to reduce the regulatory burden on businesses concerning sustainability regulations.

Amendments to the CSRD and CSDDD directives

The Corporate Sustainability Reporting Directive (CSRD) and the Corporate Sustainability Due Diligence Directive (CSDDD) were amended. The original European Commission proposal within the Omnibus package reduced the number of companies affected by the CSRD by 80%, stipulating that the regulation would apply only to companies with more than 1,000 employees instead of the originally set threshold of 250 employees; the CSDDD, according to the Commission’s February proposal, was also intended to apply to firms with more than 1,000 employees.

However, the European Parliament, while negotiating its position with EU member states, went far beyond the Commission’s proposal, which will lead to an even more significant reduction in the number of companies subject to reporting and due‑diligence obligations. It is estimated that up to 90 % of firms will be excluded from the scope of the CSRD. The agreement kept the 1,000‑employee threshold but added a new net turnover threshold of 450 million EUR. For the CSDDD, the Parliament went considerably further than the European Commission’s proposal – the employee threshold was raised to 5,000 and the net turnover threshold to over 1.5 billion EUR, thereby excluding the vast majority of companies from the regulation. At the same time, the requirement for companies to prepare Climate Transition Plans (CTP) under the due‑diligence directive was abolished.

So what will apply?

Sustainability reporting obligation under the CSRD will apply only to companies with more than 1,000 employees and a net turnover above 450 million EUR.

Obligation to implement due diligence aimed at reducing negative impacts on people and the planet under the CSDDD will be required only from large EU corporations with more than 5,000 employees and a net turnover exceeding 1.5 billion EUR. The same will be required from non‑EU companies operating in the EU that exceed the same turnover threshold within the EU. Climate Transition Plans (CTP) will not be required.

According to the European Commission's proposal, the amount of information that large companies can request from smaller companies within their supply chains is also being limited. Companies with fewer than 1000 employees may refuse to provide sustainability information beyond the standards for voluntary sustainability reporting for small and medium-sized enterprises (SME reporting standard).

When will the new rules start to apply?

The European Parliament approved the new rules by a large majority of 428 votes in favour and 218 votes against. The final wording still has to be formally approved by the EU Council. The Corporate Sustainability Due Diligence Directive (CSDDD) will become effective only on 26 July 2029. The Corporate Sustainability Reporting Directive (CSRD) will be effective from January 2027, meaning companies will report in 2028 for the financial year 2027. The standards must be transposed into the legislation of EU member states.

Currently, a revision of the European sustainability reporting standards (ESRS) is also underway, and it is expected that the European Commission will adopt the revised standards in the second quarter of 2026.

Although the newly set thresholds appear to be final, the adopted text also includes the possibility of a further review of the thresholds within the CSRD and CSDDD, which concerns a possible expansion of the scope of both regulations, after four years from their entry into force. We will continue to monitor the legislation for you.

Related articles

The European Parliament approved the simplification of ESG reporting

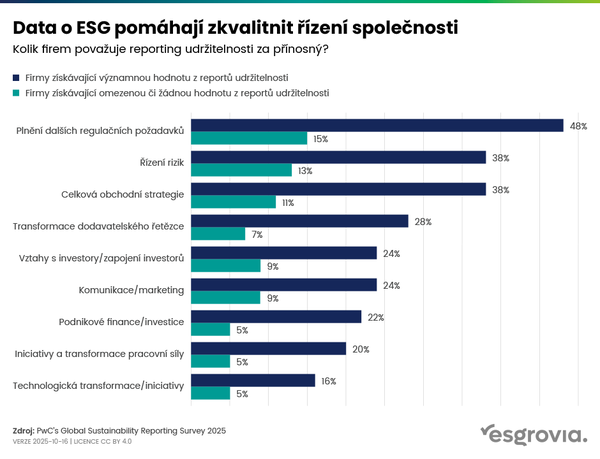

Data on ESG help improve company management

Sustainability reporting – EU back and China forward