How are Scandinavian companies preparing for the impacts of CBAM?

The Carbon Border Adjustment Mechanism (CBAM) and the EU ETS reform came into force on January 1, 2026, and for the first time in history they pass CO₂ costs directly onto the prices of European materials. Nordea Bank analyzed the impacts on Nordic companies, and the results are interesting.

Nordea estimates a price impact of up to ~20% on imports of steel, aluminium, cement and fertilizers, amounting to €80 billion in imports by 2030 — especially in the steel segment. Material producers in the EU should be the main winners thanks to higher capacity utilization and a price effect.

According to Nordea Bank, a fundamental weakness of the current setup is that CBAM does not yet cover the import of finished products made from these materials, creating a risk of circumvention and offshoring.

The European Commission proposes extending it to 180 downstream products (auto parts, household appliances, metal tools) — potentially as early as 2028. Nordea estimates the impact at around 3–5% of import value.

A survey of 40 listed Nordic firms (capital and consumer goods, construction, materials) showed that:

- material companies see CBAM as an opportunity

- construction firms assess the impact as neutral — most materials in the Nordic countries are sourced locally and

- manufacturers of capital and consumer goods see a slightly negative risk from higher input costs, especially if CBAM is extended to downstream products.

Most companies are already working on mitigation measures — primarily shifting resources to EU suppliers instead of non‑European ones.

The baseline scenario of Nordea Bank is that the current design of CBAM will essentially remain unchanged until 2030, but pressure to weaken the policies is growing and requires close monitoring.

Related articles

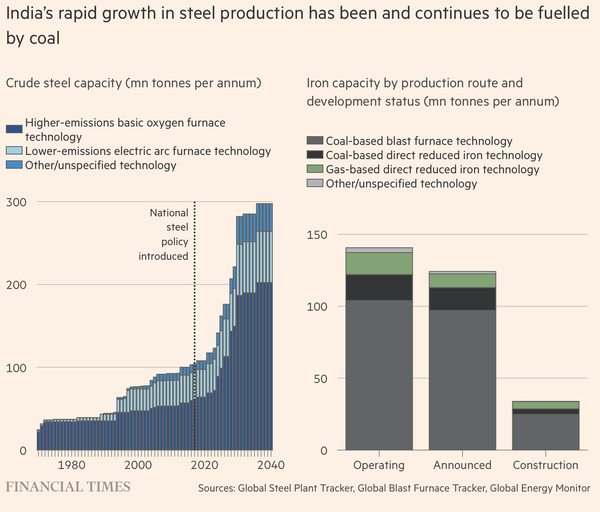

India is experiencing a steel boom, but with a high climate price tag

Carbon tax (CBAM) as a test of the EU's negotiating power