The European Parliament approved the simplification of ESG reporting

The European Parliament approved on Thursday, 13 November 2025, its negotiating position on the package of amendments referred to as “Omnibus I”, which simplifies sustainability reporting requirements and the introduction of due‑diligence principles for companies. The adopted proposal brings significant simplification for firms.

According to the MEPs, sustainability reporting should apply only to large enterprises that have on average more than 1,750 employees and an annual net turnover exceeding €450 million. Only these companies would also be subject to the reporting obligation under the EU Taxonomy rules.

The Parliament also calls for significant simplification of sustainability reporting standards, particularly by reducing qualitative requirements and introducing voluntary sector‑specific reporting. Smaller firms should then be shielded from reporting demands by their large business partners, who would not be allowed to request more information than is stipulated in the voluntary standard (VSME).

In the area of due diligence, the requirements would apply only to large firms with more than 5,000 employees and a net annual turnover exceeding €1.5 billion. These companies would no longer have to prepare a transition plan to align their business model with the Paris Agreement, and they would also not needlessly demand information from smaller business partners. For the purpose of obtaining value‑chain information, firms should rely primarily on data that is already available.

The vote on these changes saw 382 MEPs in favour, 249 against and 13 abstentions. Among the Czech MEPs, all voted for the changes except Markéta Gregorová.

The European Parliament, in its opinion, further narrowed the scope of companies that, according to the European Commission’s proposal, would be required to report on their sustainability stance. The Commission had set the threshold for reporting obligations at more than 1,000 employees and an annual net turnover above €450 million. Regarding the CSDDD directive, the European Parliament confirmed the EU Council’s position.

According to European Parliament officials, the final legislation should be completed by the end of 2025.

Sources: European Parliament, 2025; European Council, 2025.

The proposal to raise the threshold from 1,000 to 1,750 employees means a further narrowing of the circle of companies that will be required to report on sustainable development and that will have to adapt their operations to sustainability requirements.

On the other hand, sustainability data presentation requirements are becoming a natural part of supplier‑customer relationships even outside EU regulation, and this trend will certainly continue.

However, the European Parliament's position does not represent the final outcome. The proposed threshold values will still be subject to further negotiations within EU bodies and national governments, so the approval of the final legislation can be expected only in 2026.

Related articles

EU approved new sustainability reporting rules

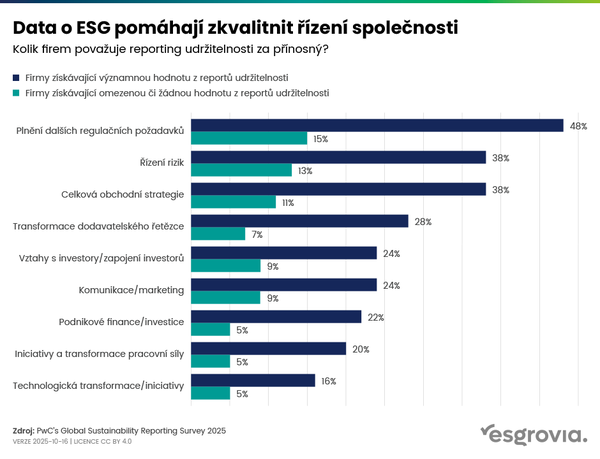

Data on ESG help improve company management

Sustainability reporting – EU back and China forward