The UK is introducing its own standards for sustainability reporting

The United Kingdom has published new UK Sustainability Reporting Standards (UK SRS), which are based on the global ISSB standards (IFRS S1 and S2).

- The FCA proposes mandatory use for listed companies from accounting periods starting on 1 January 2027

- Climate disclosure under UK SRS S2 (without Scope 3) will be strictly mandatory from day one. Scope 3 and broader sustainability reporting under S1 will be on a “comply or explain” basis.

- Unlike the global ISSB, the UK does not provide any deferral period — sustainability reports must be published alongside the financial statements already in the first reporting cycle.

- Companies without a disclosed climate transition plan will have to explain why

- Large private companies should also prepare — the British government plans to consult on their inclusion in the mandatory regime in 2026

ISSB standards are becoming a global foundation that both UK SRS and the European CSRD/ESRS are built upon. Companies reporting for international investors or partners will increasingly be confronted with the demand for comparable, auditable data across jurisdictions.

Thus, despite leaving the EU, the United Kingdom is introducing sustainability regulation similar to that of the EU and many other countries, moving us toward a globally comparable framework.

Source:

www.erm.com

Source: https://www.erm.com/

Related articles

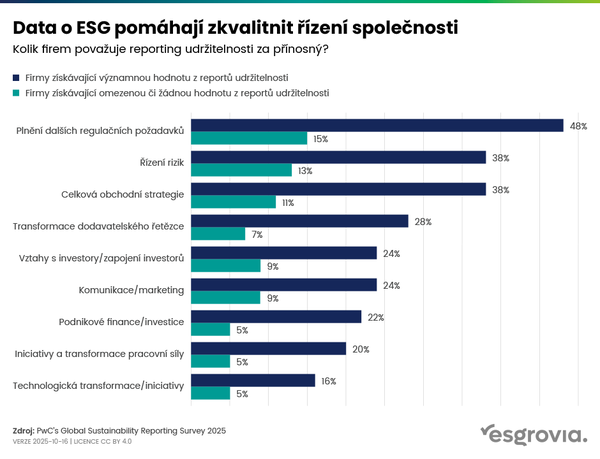

Data on ESG help improve company management

90 % of companies outside CSRD plan to continue sustainable reporting.